Generate digital cheque/DD through ATM/Internet Banking/Mobile Banking/SMS

PCT Application Number : PCT/IB2018/055035

Indian Patent Application Number : 201741025886

US Patent Application Number : Will update soon

A negotiable instrument (also sometimes referred to as banking instrument) is a document guaranteeing the payment of a specific amount of money, either on demand, or at a set time, with the payer named on the document. More specifically, it is the document contemplated by or consisting of a contract, which promises the payment of money without condition, which may be paid either on demand or at a future date. The term can have different meanings, depending on what law is being applied and what country it is used in and what context it is used in. Most widely used negotiable instruments, amongst others, are Cheque and Demand draft (DD) and both of them are mechanisms used to make payments. The cheque is a bill of exchange drawn on a specified banker and not expressed to be payable otherwise than on demand, whereas, the demand draft is a pre-paid negotiable instrument, wherein the drawee/Payer bank acts as guarantor to make payment in full when the instrument is presented. In a financial transaction, cheque is not usually accepted as the drawer and payee are unknown and there will be credit risk. So, in such cases DD is accepted where the transfer of money is guaranteed.

Indian Patent Application Number : 201741025886

US Patent Application Number : Will update soon

A negotiable instrument (also sometimes referred to as banking instrument) is a document guaranteeing the payment of a specific amount of money, either on demand, or at a set time, with the payer named on the document. More specifically, it is the document contemplated by or consisting of a contract, which promises the payment of money without condition, which may be paid either on demand or at a future date. The term can have different meanings, depending on what law is being applied and what country it is used in and what context it is used in. Most widely used negotiable instruments, amongst others, are Cheque and Demand draft (DD) and both of them are mechanisms used to make payments. The cheque is a bill of exchange drawn on a specified banker and not expressed to be payable otherwise than on demand, whereas, the demand draft is a pre-paid negotiable instrument, wherein the drawee/Payer bank acts as guarantor to make payment in full when the instrument is presented. In a financial transaction, cheque is not usually accepted as the drawer and payee are unknown and there will be credit risk. So, in such cases DD is accepted where the transfer of money is guaranteed.

The existing

payment transaction systems revolves around a few methods such as online

transfer for instant transfer of funds, making payment through banking

instruments like cheques, DDs, etc. In case of banking instruments where the

payment order is a deferred payment order, the preferred transaction mode is

through cheque where the payer's account is not debited until the cheque is

presented to a drawing bank.

Today, most of the

account holders carry physical cheques, cheque books, DD forms, and/or DDs for

making transactions. Accordingly, millions of cheque books or DD forms are

required to be printed by each bank per year costing various environmental

issues like tree cutting for generating papers or pollution while generating

cheque books or DD forms and/or printing papers. Banks are investing millions

only for printing the DD/cheque books and processing. Accordingly, in order to

compensate, customers of the bank have to pay money for the usage and

processing of the DD/cheque books and also to order for new printed DD/cheque

books to the bank. Further, with growth, development and advancement of

technology and intellect skills of the people, forgery cases, by manipulating

(signature, amount etc. on the cheque or DD), are increasing day by day for DDs

and/or cheques. Furthermore, in case of forgery cases or fraud, several

civil/criminal investigations are required to recover the original money which

is a time consuming process.

Irrespective of these

drawbacks, currently, the DD and cheque transactions are nearly impossible

without paper printing. The existing mechanisms requires numerous pieces of

paper to be passed from bank to customer, in blank, and then from customer to

payee and then from payee to their own bank for processing through the

inter-bank clearing system for subsequent proofing and payment. These steps are

inefficient and resource intensive and value exchange can be better undertaken

through more innovative methods.

As more financial

transactions are performed electronically, there is a need for facilitating

transactions without the need for currency or cash. Additionally, it is often

cumbersome to carry a wallet or purse with a cheque book, credit cards, cash

cards, or currency. However, most people carry a mobile phone or communication

device almost all the time. Therefore, it would be advantageous to provide a

way to utilize a mobile phone or communication device to conduct transactions

between two parties while avoiding the need for physical cash currency, credit

cards, or cheque books.

While there exists

many electronic cheques (e-cheque)/DDs based transaction systems to solve most

of the above mentioned problems available in the present market, however, they

fail to provide an advanced technical solution for achieving a secure

transaction as e-cheque/DD can be easily retrieved or obtained from the payee

or the payer.

Therefore, there

still exists a dire need to provide a new, technically advanced and improved

system and method enables for real-time generation of electronic negotiable

instrument, such as cheque and demand draft (DD), for secure money transfer,

payment and management thereof. More over this improved advanced system is

proposed based on the present available technologies which means users can

utilize their mobile devices or computers to generate the electronic negotiable

instruments. i.e users can generate using internet banking, Mobile apps, ATM

and also through simple SMS.

How it works:

The overall

process is in four phases:

1. Generate the

e-cheque/DD

2. Share the same

with beneficiary

3. Clearing the e-cheque/DD

4. Cancel the e-cheque/DD

It should be

appreciated that 3 OTP’s are generated during the overall implementation,

working and processing of the requests received from payer and/or payee during

the generation and/or clearance of e-cheque/DD. At least first of the 3 OTP’s

may be referred to as a first OTP/OTP 1/ Unique Cheque Request Number (UCRQN) /

Unique Demand Draft Request Number (UDDRQN). At least second of the 3 OTP’s may

be referred to as a second OTP/OTP 2/ Unique Cheque Reference Number (UCRFN) /

Unique Demand Draft Reference Number (UDDRFN). At least third of the 3 OTP’s

may be referred to as a third OTP/OTP 3/Unique Cheque Clearance Number (UCCN) /

Unique Demand Draft Clearance Number (UDDCN).

Generate the

e-cheque/DD:

The process for

generating the e-cheque/DD using internet banking can include the following

steps: customer/payer logs into his/her mobile/internet banking portal and

selects a “Generate E-cheque/DD” from menu/item/option; the customer then

select either e-cheque/DD option (it may be appreciated that, the details

filling form may be different for e-DD and e-cheque); The customer then fills

one or more details such as but not limited to his/her account details,

e-cheque/DD date, type of e-cheque to be generated, beneficiary/payee details

including but not limited to payee/beneficiary/FIRM name, bank name/IFSC code,

account number, and mobile number; the payer then enters a desired amount; and

after filling all the required details, finally, clicks on

generate/submit/proceed button; in response to the selection of the

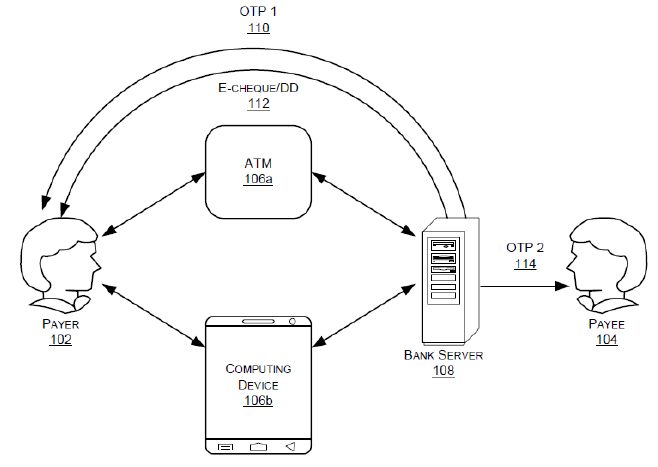

generate/submit/proceed button, OTP 1 is sent to the payer; after successful

insertion of the OTP 1 of the payer and an additional CVV number or first four

digits of debit card or any customized number is entered and then click on

confirm button. Upon verification of both OTP 1 and additional security code,

an e-cheque/DD (that may include but not limited to QR code/ Barcode or any

other security code) is generated along with watermarked bank name (as

background image) on e-cheque/DD, there can be an option provided to have the

payer/customer signature on e-cheque but this is not mandatory; then the

e-cheque/DD generated is sent to the payer’s registered email address in

JPEG/PNG/PDF or any other digital formats and at the same time and OTP 2 is

sent to the payee’s mobile number (the mobile number is entered in the e-cheque/DD

generation details). The payer shares the received e-cheque/DD with the payee

through email/Whatsapp or by any other digital communication platform.

The process for

generating the e-cheque/DD using ATM consists of following steps: payer visits

the ATM and inserts his/her Debit card and authenticates himself/herself with

the PIN; selects a “Generate E-cheque/DD” option from user interface of the

ATM; the customer then select either e-cheque or e-DD option (it may be

appreciated that, the details filling form may be different for e-DD and

e-cheque); enters payee/beneficiary/FIRM name, bank account number, bank

name/IFSC code and mobile number; enter a desired amount; clicks on

“Generate/Submit/Proceed” button from user interface of the ATM; OTP 1 is sent

to the payer; after successful insertion of the OTP 1 of the payer and an

addition CVV number or first four digits of debit card or any customized number

and then click on confirm button. Upon verification of both OTP 1 and

additional security code, an e-cheque/DD (that may include but not limited to

QR code/ Barcode or any other security code) is generated along with

watermarked bank name (as background image) on e-cheque/DD, there can be an

option provided to have the payer/customer signature on e-cheque but this is

not mandatory; then the e-cheque/DD generated is sent to the payer’s registered

email address in JPEG/PNG/PDF or any other digital formats and at the same time

and OTP 2 is sent to the payee’s mobile number (the mobile number is entered in

the e-cheque/DD generation details). The payer shares the received e-cheque/DD

with the payee through email/Whatsapp or by any other digital communication platform.

The

process to generate an e-cheque/e-DD through an SMS (message) by a payer. The

payer may send a SMS from payers’ registered mobile number to the bank SMS

server and then bank server will process the request. An OTP 1 will be received

by the payer and then payer may send the OTP 1 received as SMS to the bank SMS

server again, for example otpv <otp1>, to bank SMS server. The bank

server finally validates the beneficiary and OTP 1 details and then

e-cheque/e-DD will be generated. The e-cheque/e-DD generated is then sent to

payer registered email address. While the generation of e-cheque/e-DD an OTP 2

is sent to payees’ mobile number which is included in the SMS syntax. The payer

may then share the generated e-cheque/e-DD with the payee. In an exemplary

embodiment, the SMS sent to bank server may be of below syntax:

GenEchq/edd

<last 4 digits of debit card> <pin> <cheque type> <payee

name> <payeemobile number> <payee account number> <payee ifsc

code> <amount>

The process for

clearing the e-cheque/DD by visiting a bank consists of following steps: the

payee shares the e-cheque/DD along with the OTP 2 to a bank employee/teller.

The bank employee processes/verifies the e-cheque/DD by reading QR code/barcode

(or any other security codes) available/written on the e-cheque/DD along with

the OTP 2. While clearing the e-cheque/DD, OTP 3 is received by the payee and

is shared with the bank employee such that he/she can successfully process and

clear the e-cheque/DD upon verification. The amount is credited to the payee’s

bank account, or cash is given if e-cheque is made for self.

The process for

clearing the e-cheque/DD by visiting an ATM consists of following steps: the

payee visits an ATM and chooses “Clear e-cheque/DD option” from the user

interface of the ATM; the customer then select either e-cheque or e-DD option;

places the QR code/ Barcode (or any other security codes) of the e-cheque/DD

under QR/Bar code or any other security code scanner device at the ATM; the

scanner reads all details from the e-cheque/DD and auto fills a corresponding

form; payee checks the details on the screen, if all the values are correct

then enter/presents OTP 2 received by the payee to validate the e-cheque/DD;

while the verification of the e-cheque/DD and OTP 2, OTP 3 is generated by the

bank server and is received by the payee. Once the payee enters OTP 3 and

clicks on confirm button/option, upon verification of the e-cheque/DD, OTP 2

and OTP 3 e-cheque/DD is cleared. The amount is credited to the payee’s bank

account, or cash is dispensed by the ATM if e-cheque is made for self.

An

aspect of the present disclosure relates to clearance of e-cheque/e-DD through

an SMS (message) by a payee. First the payee sends a SMS (from mobile number

which is provided while e-cheque/e-DD generation) with the e-cheque/e-DD number

along with the mobile number (provided while generating e-cheque/e-DD) and the

OTP 2. In an example, the SMS (message) may have syntax as:

Clrchq/clrdd

<echeque/dd number> <mobile number> <otp2>.

Once

send the above SMS by the payee, an OTP 3 will be received by the payee from

the bank server. If payee wants to clear the e-cheque/e-DD without visiting

bank or ATM then simply payee sends SMS with the OTP 3 to bank SMS server as

example PRSCHQ/DD <otp3>. If the cheque is made for account payee then

the amount will be credited into payee bank account automatically. If the

cheque is for self and then skip the above process (sending OTP 3 to bank SMS

server) and enter the otp3 in the ATM to dispense the amount. In case of payee

decides to clear the cheque using ATM, then in the ATM user can see one more

option to clear the cheque by SMS then it will ask to enter otp3 after

validation the desired amount. Will be dispensed by the ATM. The SMS clearance

feature at ATM is only valid for self cheques but not other types of cheques.

Cancelling

the e-cheque/DD:

The process for

cancelling the generated e-cheques/DDs through mobile/internet banking consists

of following steps: payer logs into the user bank account through mobile

app/internet banking; selects a cancel e-cheque/DD option; selects either

e-cheque or e-DD option; enter the e-cheque/DD number; if multiple

e-cheques/DDs to be cancelled then enter each e-cheque/DD number separated by

comma. Ex: 11111, 2222, 4444 etc.; while processing cancellation request an

Unique Cheque Cancel Request Number (UCCRN)/Unique DD cancellation Request

Number (UDDCRN) will be sent to a registered mobile number of login account

holder or person who generated the cheque/DDs; payer enters the UCCRN/UDDCRN

and click on confirm; the e-cheques/DDs will be cancelled automatically; upon

cancellation an SMS will be sent to the each payee’s mobile number (person

whose mobile number is included while creating the e-cheque/DD) saying that

“The e-cheque/DD with <NUMBER> is cancelled”; cancellation process

completed. In another aspect, the multiple e-cheques/DDs cancellation process

can be treated and performed as a single transaction.

The process for

cancelling the generated e-cheques/DD through ATM consists of following steps:

payer authenticate with debit/credit card and PIN at the ATM; selects a cancel

e-cheque/DD option; the customer then select either e-cheque or e-DD option;

enter the e-cheque/DD number; if multiple e-cheques to be cancelled then enter

each e-cheque/DD number separated by comma. Ex: 11111, 2222, 4444 etc.; while

processing cancellation request an Unique Cheque Cancel Request Number

(UCCRN)/Unique DD cancellation Request Number (UDDCRN) will be sent to a

registered mobile number of login account holder or person who generated the

e-cheque/DD; payer enters the UCCRN/UDDCRN and click on confirm; the

e-cheque/DD will be cancelled automatically; upon cancellation an SMS will be

sent to the each payee’s mobile number (person whose mobile number is included

while creating the e-cheque/DD) saying that “The cheque/DD with <NUMBER>

is cancelled”; cancellation process completed. In another aspect, the multiple

e-cheques/DDs cancellation process can be treated and performed as a single

transaction.

Please provide me your valuable suggestions and comments on this article.

Reach me @ my.innovationconcepts@gmail.com

Disclaimer: Chances are there that some one may have patents on the similar innovative ideas but all these concepts are my own individual thoughts.

Thanks,

SPCS

Please provide me your valuable suggestions and comments on this article.

Reach me @ my.innovationconcepts@gmail.com

Disclaimer: Chances are there that some one may have patents on the similar innovative ideas but all these concepts are my own individual thoughts.

Thanks,

SPCS

Comments

Post a Comment